Cleaning Anomalies to Reduce Forecast Error by 9% with anomalize

Written by Matt Dancho

In this tutorial, we’ll show how we used clean_anomalies() from the anomalize package to reduce forecast error by 9%.

R Packages Covered:

anomalize - Time series anomaly detection

Cleaning Anomalies to Reduce Forecast Error by 9%

We can often improve forecast performance by cleaning anomalous data prior to forecasting. This is the perfect use case for integrating the clean_anomalies() function from anomalize into your forecast workflow.

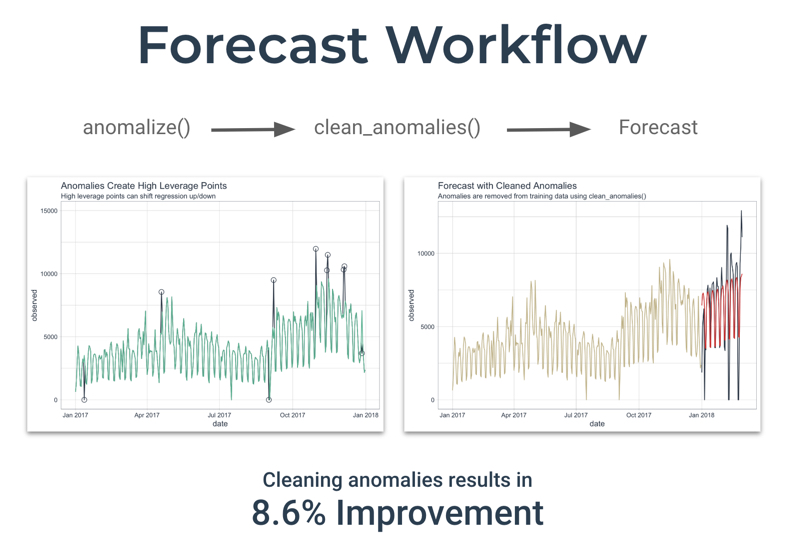

Forecast Workflow

We’ll use the following workflow to remove time series anomalies prior to forecasting.

-

Identify the anomalies - Decompose the time series with time_decompose() and anomalize() the remainder (residuals)

-

Clean the anomalies - Use the new clean_anomalies() function to reconstruct the time series, replacing anomalies with the trend and seasonal components

-

Forecast - Use a forecasting algorithm to predict new observations from a training set, then compare to test set with and without anomalies cleaned

Step 1 - Load Libraries

First, load the following libraries to follow along.

library(tidyverse) # Core data manipulation and visualization libraries

library(tidyquant) # Used for business-ready ggplot themes

library(anomalize) # Identify and clean time series anomalies

library(timetk) # Time Series Machine Learning Features

library(knitr) # For kable() function

Step 2 - Get the Data

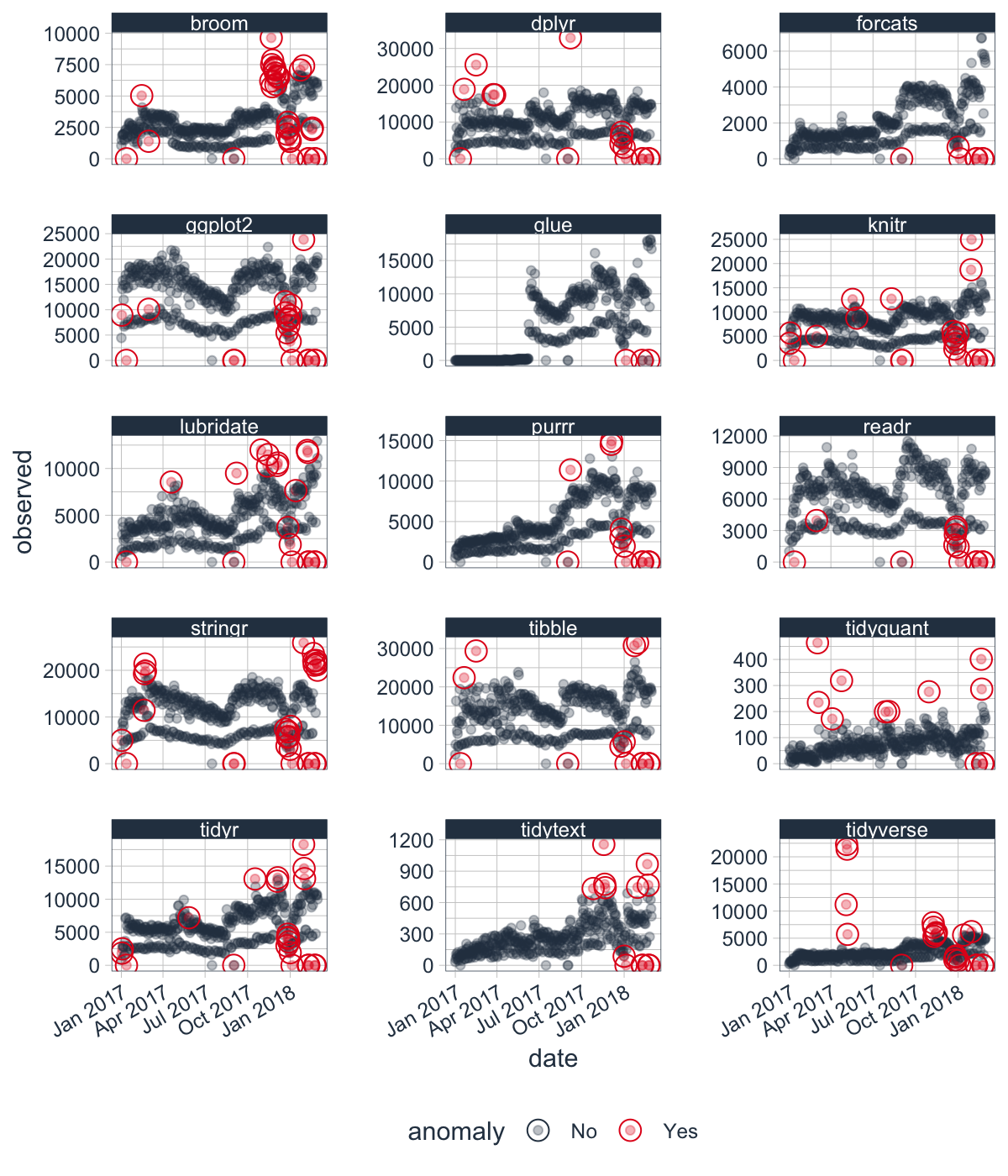

This tutorial uses the tidyverse_cran_downloads dataset that comes with anomalize. These are the historical downloads of several “tidy” R packages from 2017-01-01 to 2018-03-01.

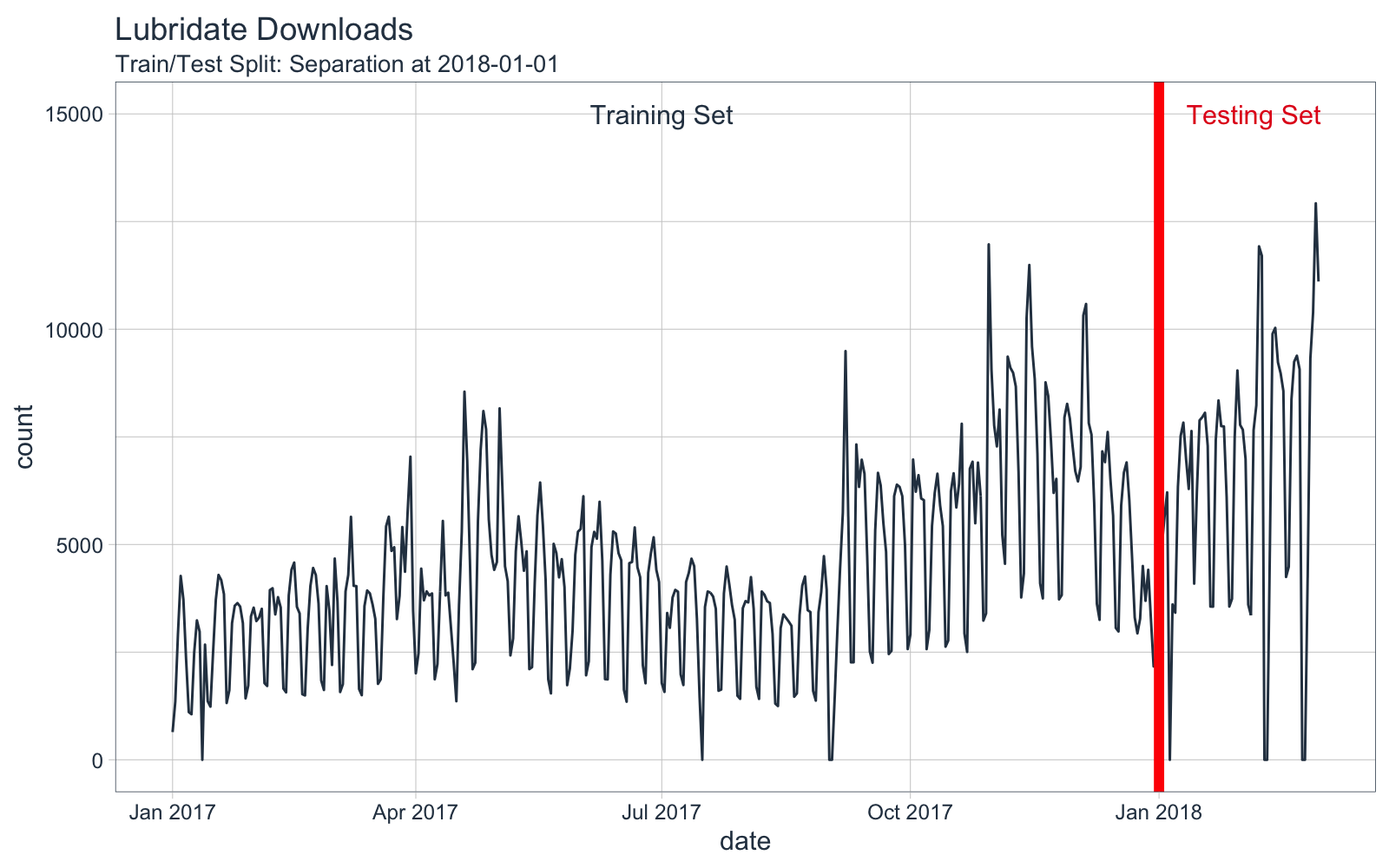

Let’s take one package with some extreme events. We’ll hone in on lubridate (but you could pick any).

tidyverse_cran_downloads %>%

time_decompose(count) %>%

anomalize(remainder) %>%

time_recompose() %>%

plot_anomalies(ncol = 3, alpha_dots = 0.3)

We’ll filter() downloads of the lubridate R package.

lubridate_tbl <- tidyverse_cran_downloads %>%

ungroup() %>%

filter(package == "lubridate")

Here’s a visual representation of the forecast experiment setup. Training data will be any data before “2018-01-01”.

Step 3 - Workflow for Cleaning Anomalies

The workflow to clean anomalies:

-

We decompose the “counts” column using time_decompose() - This returns a Seasonal-Trend-Loess (STL) Decomposition in the form of “observed”, “season”, “trend” and “remainder”.

-

We fix any negative values - If present, they can throw off forecasting transformations (e.g. log and power transformations)

-

We identifying anomalies (anomalize()) on the “remainder” column - Returns “remainder_l1” (lower limit), “remainder_l2” (upper limit), and “anomaly” (Yes/No).

-

We use the function, clean_anomalies(), to add new column called “observed_cleaned” that repairs the anomalous data by replacing all anomalies with the trend + seasonal components from the decompose operation.

lubridate_anomalized_tbl <- lubridate_tbl %>%

# 1. Decompose download counts and anomalize the STL decomposition remainder

time_decompose(count) %>%

# 2. Fix negative values if any in observed

mutate(observed = ifelse(observed < 0, 0, observed)) %>%

# 3. Identify anomalies

anomalize(remainder) %>%

# 4. Clean & repair anomalous data

clean_anomalies()

# Show change in observed vs observed_cleaned

lubridate_anomalized_tbl %>%

filter(anomaly == "Yes") %>%

select(date, anomaly, observed, observed_cleaned) %>%

head() %>%

kable()

| date |

anomaly |

observed |

observed_cleaned |

| 2017-01-12 |

Yes |

0 |

3522.194 |

| 2017-04-19 |

Yes |

8549 |

5201.716 |

| 2017-09-01 |

Yes |

0 |

4136.721 |

| 2017-09-07 |

Yes |

9491 |

4871.176 |

| 2017-10-30 |

Yes |

11970 |

6412.571 |

| 2017-11-13 |

Yes |

10267 |

6640.871 |

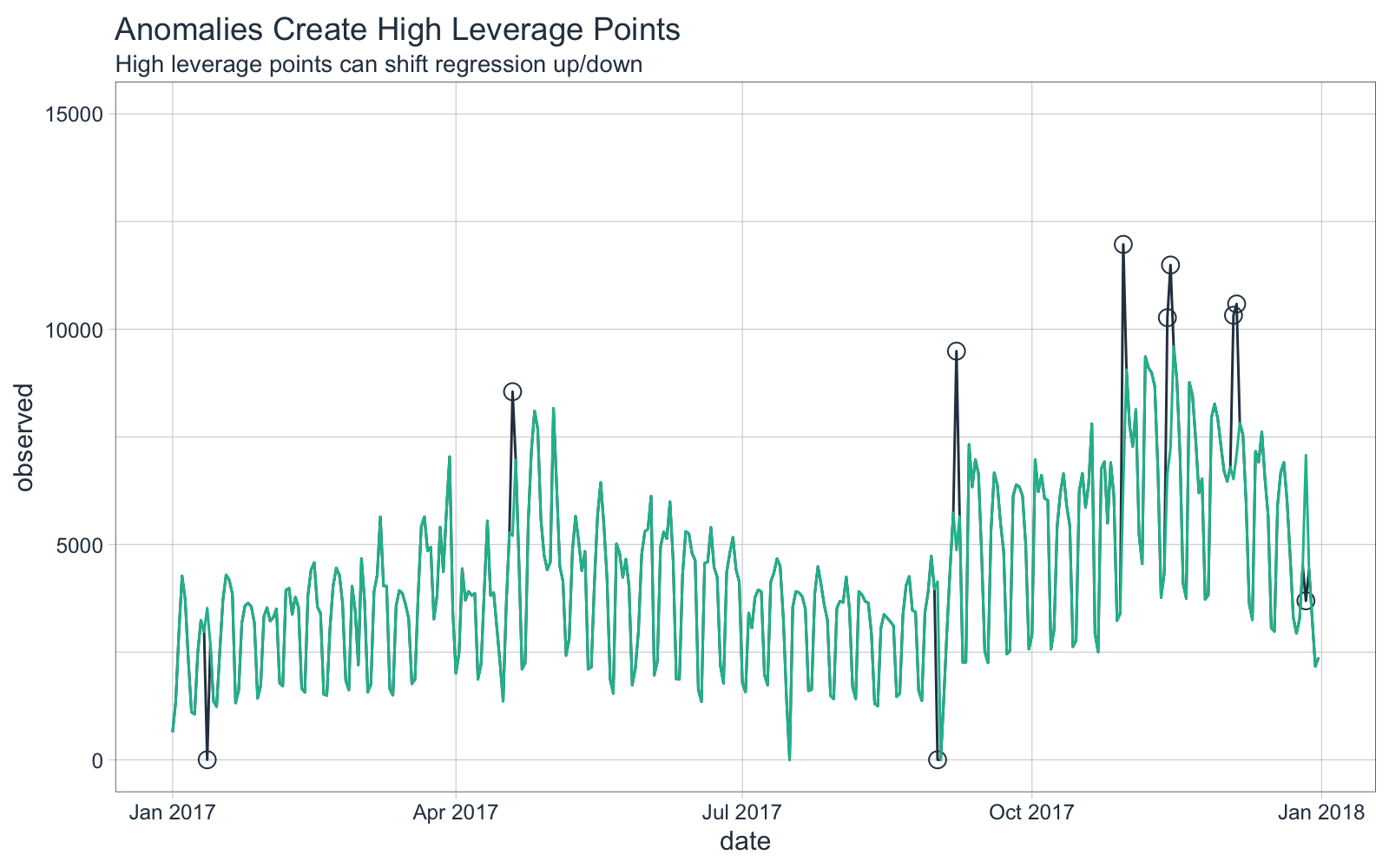

Here’s a visual of the “observed” (uncleaned) vs the “observed_cleaned” (cleaned) training sets. We’ll see what influence these anomalies have on a forecast regression (next).

Step 4 - Forecasting Downloads of the Lubridate Package

First, we’ll make a function, forecast_downloads(), that can take the input of both cleaned and uncleaned anomalies and return the forecasted downloads versus actual downloads. The modeling function is described in the Appendix - Forecast Downloads Function.

Step 4.1 - Before Cleaning with anomalize

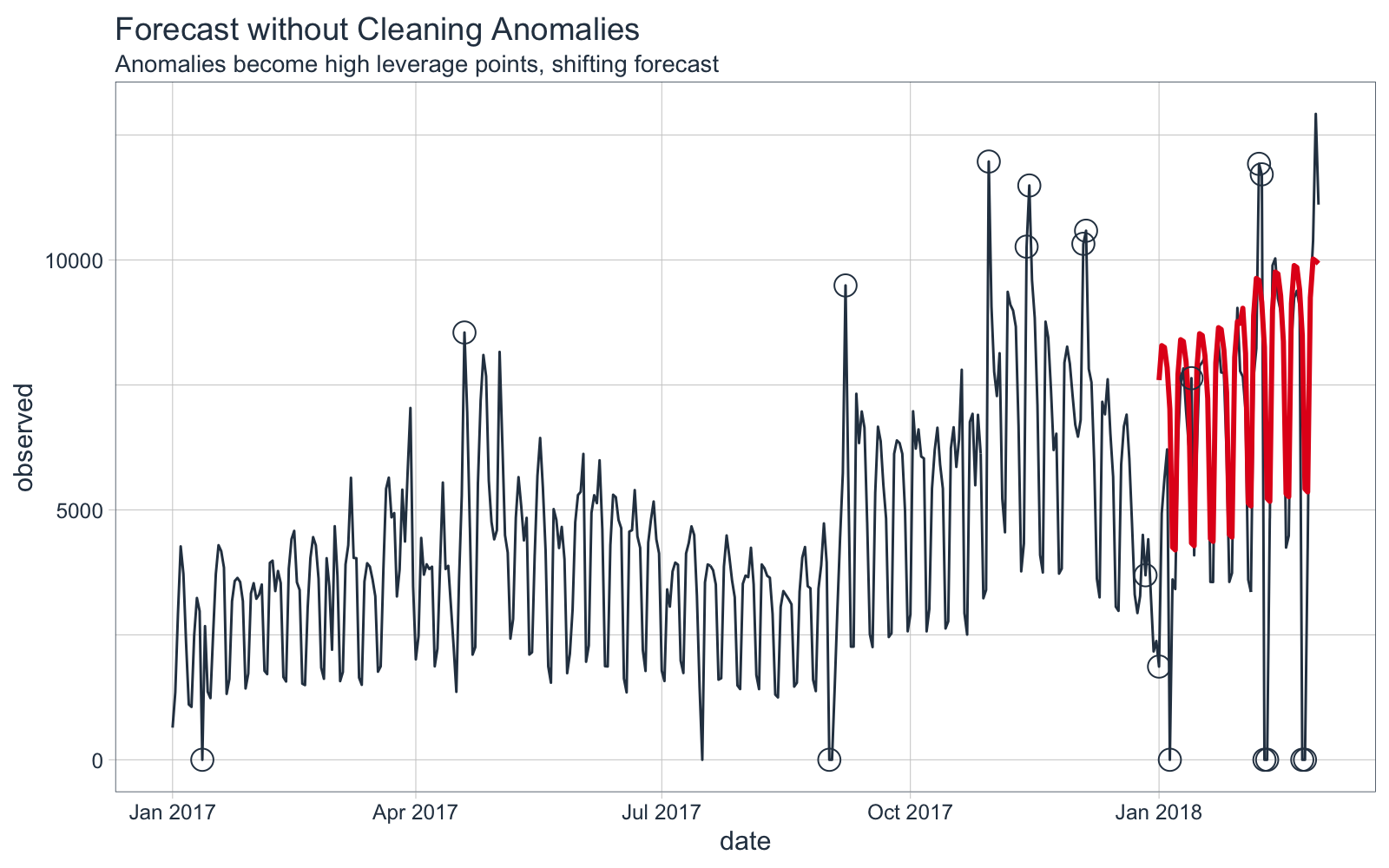

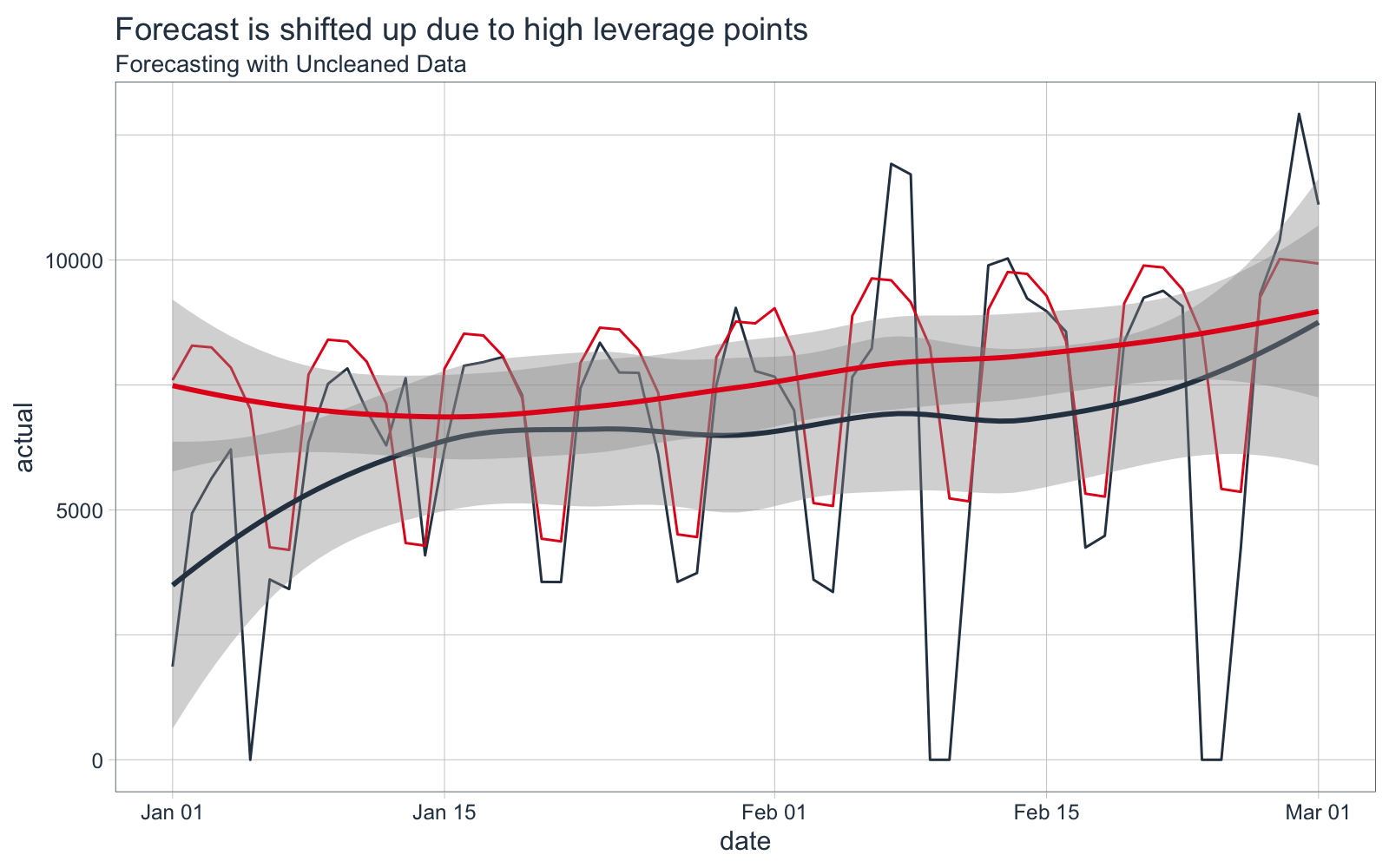

We’ll first perform a forecast without cleaning anomalies (high leverage points).

- The

forecast_downloads() function trains on the “observed” (uncleaned) data and returns predictions versus actual.

- Internally, a power transformation (square-root) is applied to improve the forecast due to the multiplicative properties.

- The model uses a linear regression of the form

sqrt(observed) ~ numeric index + year + quarter + month + day of week.

lubridate_forecast_with_anomalies_tbl <- lubridate_anomalized_tbl %>%

# See Apendix - Forecast Downloads Function

forecast_downloads(

col_train = observed, # First train with anomalies included

sep = "2018-01-01", # Separate at 1st of year

trans = "sqrt" # Perform sqrt() transformation

)

Forecast vs Actual Values

The forecast is overplotted against the actual values.

We can see that the forecast is shifted vertically, an effect of the high leverage points.

Forecast Error Calculation

The mean absolute error (MAE) is 1570, meaning on average the forecast is off by 1570 downloads each day.

lubridate_forecast_with_anomalies_tbl %>%

summarise(mae = mean(abs(prediction - actual)))

## # A tibble: 1 x 1

## mae

## <dbl>

## 1 1570.

Step 4.2 - After Cleaning with anomalize

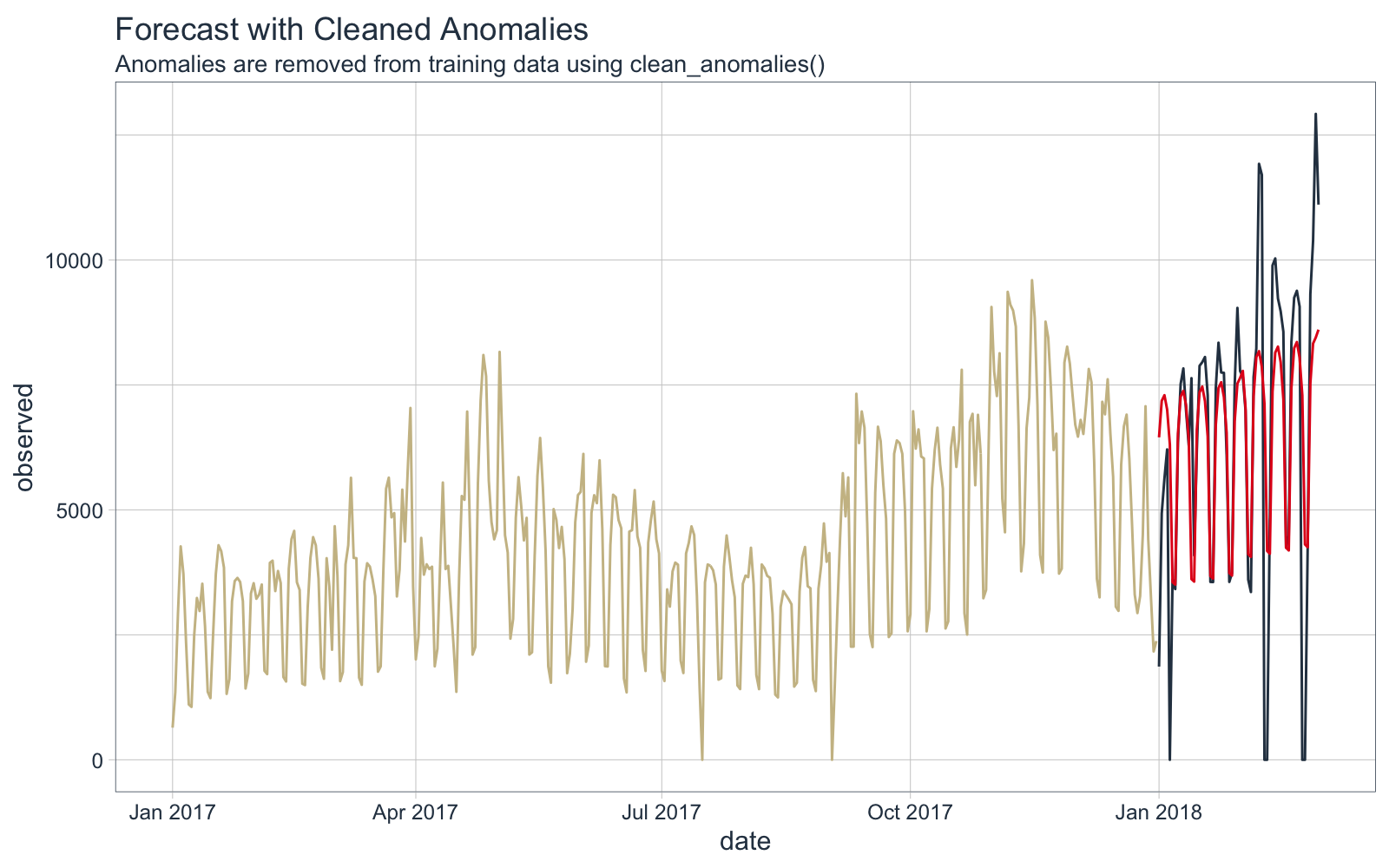

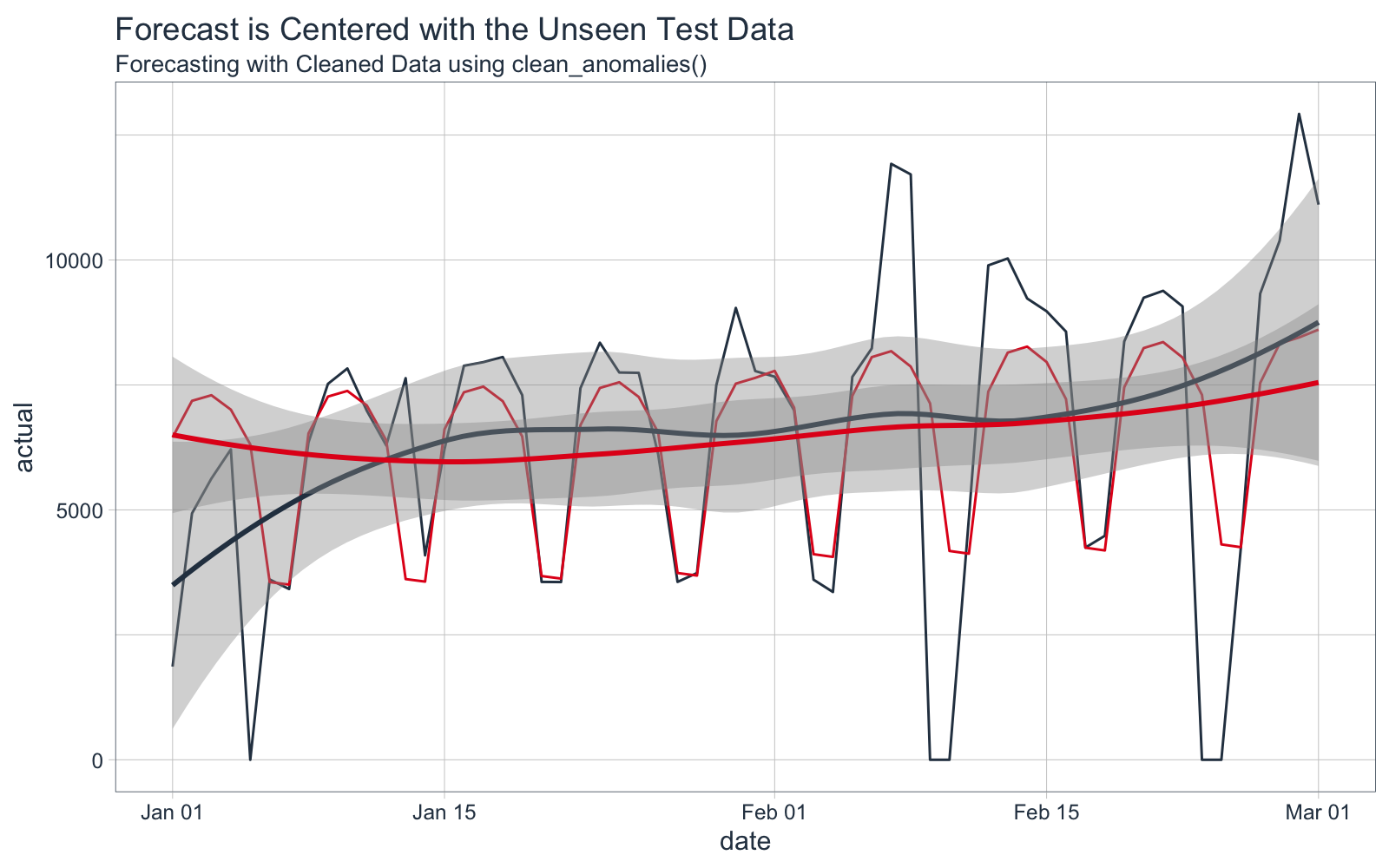

We’ll next perform a forecast this time using the repaired data from clean_anomalies().

- The

forecast_downloads() function trains on the “observed_cleaned” (cleaned) data and returns predictions versus actual.

- Internally, a power transformation (square-root) is applied to improve the forecast due to the multiplicative properties.

- The model uses a linear regression of the form

sqrt(observed_cleaned) ~ numeric index + year + quarter + month + day of week

lubridate_forecast_without_anomalies_tbl <- lubridate_anomalized_tbl %>%

# See Appendix - Forecast Downloads Function

forecast_downloads(

col_train = observed_cleaned, # Forecast with cleaned anomalies

sep = "2018-01-01", # Separate at 1st of year

trans = "sqrt" # Perform sqrt() transformation

)

Forecast vs Actual Values

The forecast is overplotted against the actual values. The cleaned data is shown in Yellow.

Zooming in on the forecast region, we can see that the forecast does a better job following the trend in the test data.

Forecast Error Calculation

The mean absolute error (MAE) is 1435, meaning on average the forecast is off by 1435 downloads each day.

lubridate_forecast_without_anomalies_tbl %>%

summarise(mae = mean(abs(prediction - actual)))

## # A tibble: 1 x 1

## mae

## <dbl>

## 1 1435.

8.6% Reduction in Forecast Error

Using the new anomalize function, clean_anomalies(), prior to forecasting results in an 8.6% reduction in forecast error as measure by Mean Absolute Error (MAE).

((1435 - 1570) / 1570)

## [1] -0.08598726

Conclusion

Forecasting with clean anomalies is a good practice that can provide substantial improvement to forecasting accuracy by removing high leverage points. The new clean_anomalies() function in the anomalize package provides an easy workflow for removing anomalies prior to forecasting. Learn more in the anomalize documentation.

Data Science Training

Interested in Learning Anomaly Detection?

Business Science offers two 1-hour labs on Anomaly Detection:

Interested in Improving Your Forecasting?

Business Science offers a 1-hour lab on increasing Forecasting Accuracy:

- Learning Lab 5 - 5 Strategies to Improve Forecasting Performance by 50% (or more) using

arima and glmnet

Interested in Becoming an Expert in Data Science for Business?

Business Science offers a 3-Course Data Science for Business R-Track designed to take students from no experience to an expert data scientists (advanced machine learning and web application development) in under 6-months.

Appendix - Forecast Downloads Function

The forecast_downloads() function uses the following procedure:

- Split the

data into training and testing data using a date specified using the sep argument.

- Apply a statistical transformation: none, log-1-plus (

log1p()), or power (sqrt())

- Model the daily time series of the training data set from observed (demonstrates no cleaning) or observed and cleaned (demonstrates improvement from cleaning). Specified by the

col_train argument.

- Compares the predictions to the observed values.

forecast_downloads <- function(data, col_train,

sep = "2018-01-01",

trans = c("none", "log1p", "sqrt")) {

predict_expr <- enquo(col_train)

trans <- trans[1]

# Spit into training/testing sets

train_tbl <- data %>% filter(date < ymd(sep))

test_tbl <- data %>% filter(date >= ymd(sep))

# Apply Transformation

pred_form <- quo_name(predict_expr)

if (trans != "none") pred_form <- str_glue("{trans}({pred_form})")

# Make the model formula

model_formula <- str_glue("{pred_form} ~ index.num + half

+ quarter + month.lbl + wday.lbl") %>%

as.formula()

# Apply model formula to data that is augmented with time-based features

model_glm <- train_tbl %>%

tk_augment_timeseries_signature() %>%

glm(model_formula, data = .)

# Make Prediction

suppressWarnings({

# Suppress rank-deficit warning

prediction <- predict(model_glm, newdata = test_tbl %>%

tk_augment_timeseries_signature())

actual <- test_tbl %>% pull(!! actual_expr)

})

if (trans == "log1p") prediction <- expm1(prediction)

if (trans == "sqrt") prediction <- ifelse(prediction < 0, 0, prediction)^2

# Return predictions and actual

tibble(

date = tk_index(test_tbl),

prediction = prediction,

actual = observed

)

}